Эконометрические

программы

Эконометрические

|

|

Econometric

|

|

Оценивание пороговой авторегрессии. Версия: 09.2005 |

Estimating threshold autoregression. Version: 09.2005 |

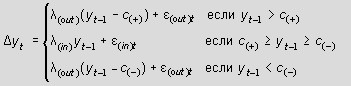

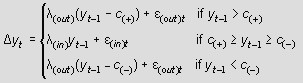

Пороговая авторегрессия (ПАР) определяется как

где y - временной ряд (t = 1,...,T). Более подробное описание модели и её приложение см. в LICOS DP No. 152/2004. Программа оценки параметров ПАР (авторегрессионных коэффициентов λ и порогов с) и тестирования на пороговый эффект реализована в виде макроса Microsoft Excel. Упакованный файл содержит инструкцию к программе (в формате pdf) и файл Excel с контрольным примером и макросом программы. |

The threshold autoregression (TAR) is specified as

where y is a time series (t = 1,...,T). See LICOS DP No. 152/2004 for more details and an application. The program for estimating TAR parameters (namely, autoregressive coefficients λ and thresholds с) and testing for the threshold effect is organized as a Microsoft Excel macro. A compressed file contains instructions (in pdf format) and an Excel file with a test example and the program macro. |

| Скачать (zip, 355 k) | Download (zip, 280 k) |

|

Нелинейный тест на единичный корень при структурном скачке среднего. Версия: 08.2005 |

Nonlinear unit root test in the presence of a structural break in the mean. Version: 08.2005 |

Пусть временной ряд y имеет структурный скачок в t = θ + 1.

Обычно для тестирования такого ряда

на единичный корень используется линейная модель Перрона -

b.jpg) (t = 1,...,T),

где (t = 1,...,T),

где .jpg) = 0, если t ≤ θ,

и = 1, если t > θ. Однако

для более точного описания процесса на коэффициенты должно быть наложено нелинейное

ограничение ψ = -λδ/(λ + 1). Такой нелинейный тест

оказывается более мощным, чем тест Перрона, причём асимптотическими распределениями

статистики нелинейного теста являются распределения Дикки-Фуллера. = 0, если t ≤ θ,

и = 1, если t > θ. Однако

для более точного описания процесса на коэффициенты должно быть наложено нелинейное

ограничение ψ = -λδ/(λ + 1). Такой нелинейный тест

оказывается более мощным, чем тест Перрона, причём асимптотическими распределениями

статистики нелинейного теста являются распределения Дикки-Фуллера.Подробности - в MPRA Paper No. 678. Программы тестирования на единичный корень, получения p-значений теста и дополнительные программы реализованы в виде программ для EViews. Материалы содержатся в двух упакованных файлах: первый включает инструкцию к программам (в формате pdf, по-английски) и сами программы, второй -- файл Excel с p-значениями тестовых статистик. |

Let a time series y has a structural break at t = θ + 1.

Commonly, to test such a series for a unit root, the Perron's linear model is used,

(t = 1,...,T),

where = 0 if t ≤ θ

and = 1 if t > θ.

However, to more adequately describe the underlying process, nonlinear constraint

ψ = -λδ/(λ + 1) should be imposed on the coefficients. Such a nonlinear

test is more powerful than the Perron test, the asymptotic distributions

of the nonlinear test statistics coinciding with the Dickey-Fuller distributions. For details, see MPRA Paper No. 678. The program for unit root testing and the program for deriving p-values of the test as well as additional ones are organized as EViews programs. Two compessed files contain the material: the first one comprises instructions (in pdf format) and the programs themselves, and the second one comprises an Excel file with p-values of the test statistics. |

|

Скачать: программы и инструкцию (zip, 410 k) файл p-значений (zip, 2.7 Mb) |

Download: programs and instructions (zip, 410 k) file of p-values (zip, 2.7 Mb) |

|

Оценка и тестирование на единичный корень моделей временных рядов с асимптотически затухающим трендом. Версия: 07.2021 |

Estimating and testing for unit root time series models with asymptotically decaying trend. Version: 07.2021 |

Авторегрессионный процесс АР(1) с нелинейным асимптотически затухающим трендом

может моделировать конвергенцию доходов, душевого ВВП, выпусков, цен/уровней

цен и т.д. в исследованиях экономического роста или паритета покупательной

способности/закона единой цены. Более подробное описание и приложение см., например, в MPRA Paper No. 99316. Конкретными видами трендов являются логарифмически-экспоненциальный, экспоненциальный и дробный. Программы оценки таких моделей и тестирования их на единичный корень, а также программы получения p-значений теста на единичный корень реализованы в виде программ для EViews. Упакованный файл ниже содержит инструкцию к программам (в формате pdf, по-английски), сами программы и файл Excel с p-значениями тестовых статистик. |

An AR(1) autoregressive process with nonlinear asymptotically decaying trend

can model convergence of incomes, GDP per capita, output, prices/price levels,

etc. in the context of economic growth or purchasing power

parity/the law of one price. See, e.g., MPRA Paper No. 99316 for details and an application. Specific forms of the trend are the log-exponential trend, exponential trend, and fractional trend. The programs for estimating such models and testing them for unit root as well as the programs for deriving p-values of the unit root test are organized as EViews programs. The compressed file below contains instructions (in pdf format), the programs themselves, and an Excel file with p-values of the test statistics. |

| Скачать (zip, 756 k) | Download (zip, 756 k) |